Blog

Is Insurance Adjusting Software Accurate?

Since I began my career in insurance adjusting in November 1999 with GAB Robins, a major national and international adjusting firm with over 300 offices, I’ve seen how insurance estimating software has evolved. As an independent adjuster, I conducted daily inspections and created damage estimates for numerous insurance companies partnered with GAB Robins to handle their claims.

One of the primary software programs adjusters use today is Xactimate. While handling claims for State Farm in 1999, I was required to use their custom State Farm Xactimate price list rather than the standard pre-set Xactimate list, which meant adjusting every line item manually to align with State Farm’s pricing structure. This experience was eye-opening, highlighting discrepancies between insurance carriers’ pricing guidelines and the zip code pre-set market pricing. (See the State Farm Xactimate price list from 1999)

In 2002, after observing how some carriers failed to compensate policyholders fairly, I became a public adjuster. Since then, I’ve dedicated my career to advocating for policyholders and providing expert insurance claim appraisals, especially after hurricanes hit Florida.

The Challenge with Xactimate Pricing Post-Hurricane

Through my work after many hurricanes in Florida, I’ve found that Xactimate pricing often fails to keep up with market conditions following major storms. After a hurricane, labor and material costs surge due to increased demand and supply shortages, driving up the cost of repairs. Unfortunately, these real-time market changes are not always truly reflected accurately in software-generated pricing, leading to estimates that don’t cover actual repair costs.

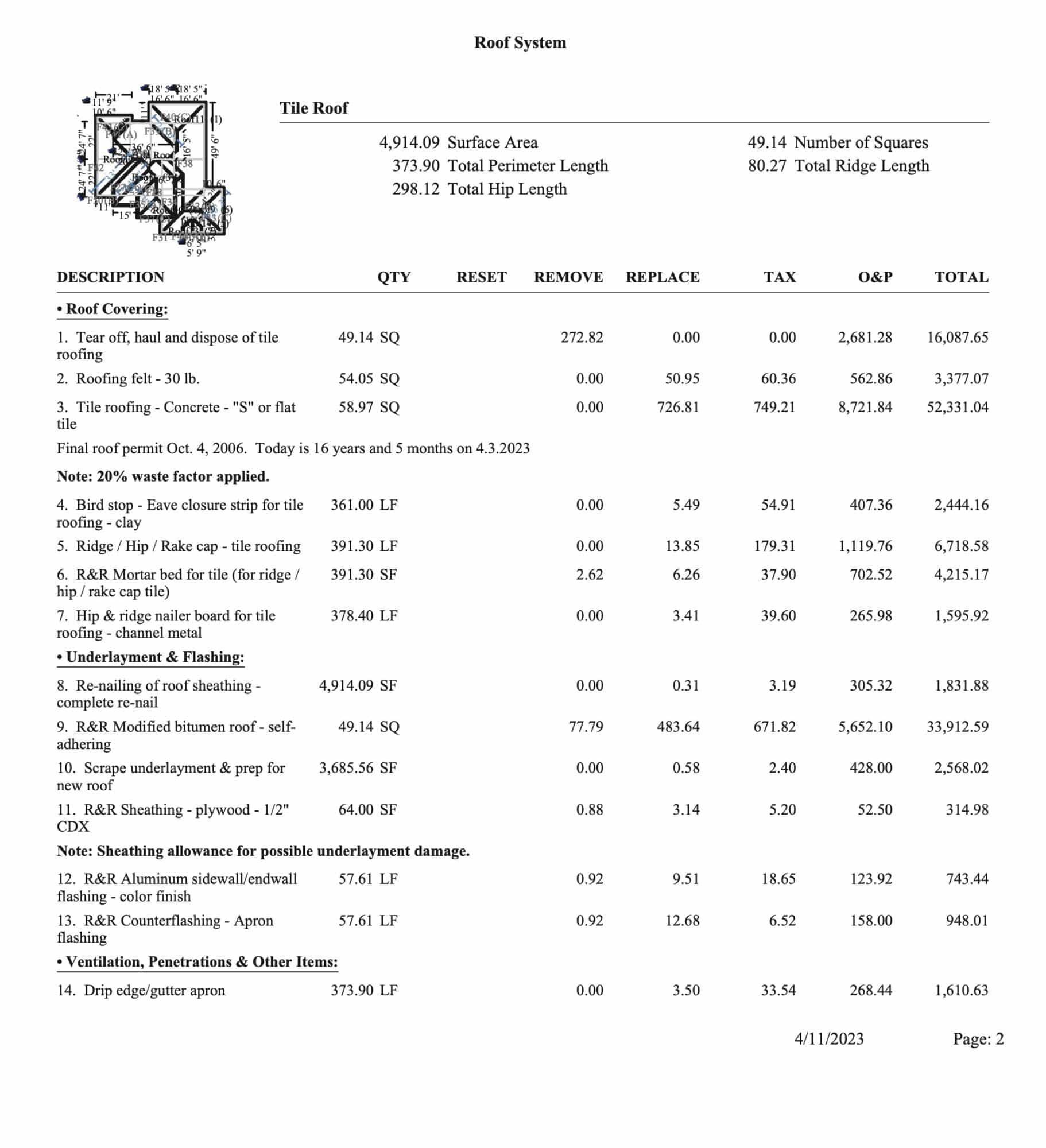

Sample of a Roof Estimate

Independent Bids vs. Software Pricing

As an experienced appraiser, I frequently prefer to obtain independent bids from local contractors, especially for high-cost or specialty repairs. In my experience, Xactimate prices can fall below what policyholders need to restore their property. Independent bids allow for a more realistic view of repair costs, ensuring policyholders have the funds to complete repairs to pre-loss conditions.

While insurance adjusting software like Xactimate is a valuable tool for estimating repair costs, it has limitations, particularly in post-disaster scenarios. Policyholders should know these estimates might not cover full repair costs and consider consulting an experienced public adjuster. With over 25 years in adjusting and construction estimating, I’m here to help ensure you receive a fair settlement.

Alternative Dispute Resolution

Residential and commercial policyholders should know that just because the insurance company sends you a settlement and insurance settlement check. The settlement can be challenged, and you do not have to accept that settlement as the full and final value of your property damage insurance claim. If the insurance company settlement offer does not allow for the complete or proper repair of your home or commercial building. There is a remedy to get a proper insurance claim settlement. There is a noncombative, fast, efficient method to challenge the disputed claim for property damages. This is called appraisal. Many Florida Insurance Companies insurance policies have insurance policy language to allow for dispute resolution thru the appraisal policy clause. The insurance company will often request the appraisal process, too. Some insurance companies prefer that you go to appraisal so they can avoid the cost of litigation, too.

Feel free to reach out and find out if your property damage insurance claim qualifies to go to appraisal for a fair insurance claim settlement. Call 1-888-554-5012 today.